Aeluma Earnings Preview

Focus on the Transition, Not the Quarter

Aeluma reports fiscal Q3 2026 results tomorrow after the close (May 13, 2026). I would caution investors against overemphasizing near-term revenue or expecting a dramatic commercial inflection point from this particular quarter.

The stock has become extremely volatile, reaching fresh all-time highs near $31 ($30.95 today) amid sharp intraday swings (currently trading ~$27 per share). With a relatively small float and growing speculative attention around photonics and heterogeneous integration, even modest commentary could drive outsized moves in either direction. That volatility increases the risk that investors focus on the wrong metrics.

The key question is not whether Aeluma suddenly posts meaningful revenue tomorrow.

The key question is whether the company continues progressing from promising technology into repeatable, manufacturable semiconductor infrastructure.

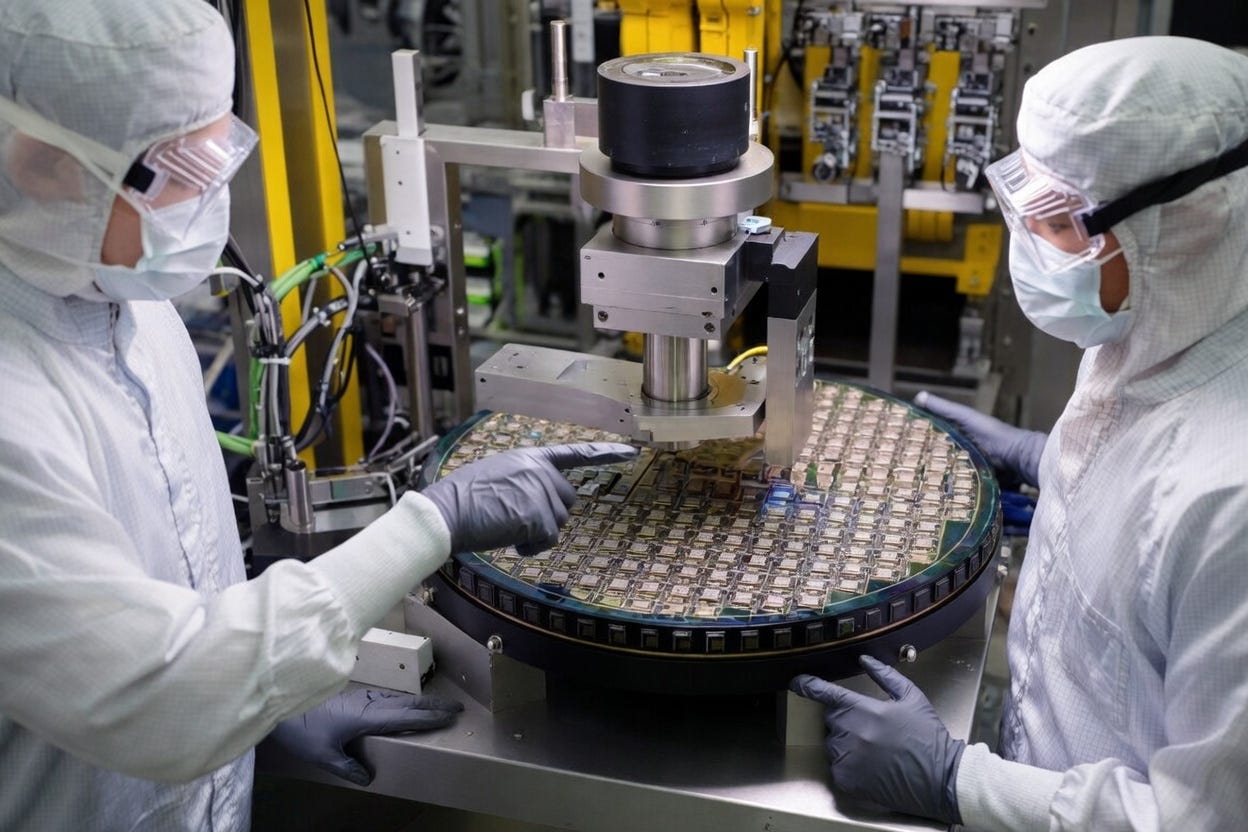

Many semiconductor companies can produce compelling lab demonstrations. Far fewer successfully achieve repeatable, foundry-compatible manufacturing flows on standard 200mm and 300mm silicon infrastructure. Aeluma’s heterogeneous integration approach is designed to bridge that gap.

That transition is rarely linear, and it almost never reveals itself through a single quarter’s financials.

What has changed over the past several months is the broader evidence stack surrounding the company. Aeluma has continued adding experienced semiconductor talent, including Willy Rachmady as VP of Strategic Partnerships, alongside personnel with deep process and manufacturing backgrounds. The company has also expanded its ecosystem relationships through partnerships and engagement with organizations such as Tower Semiconductor and Sumitomo Chemical.

Importantly, several recently announced government contracts tied to quantum dot lasers and AlGaAs materials were specifically connected to scaling efforts involving Tower and Sumitomo. Those announcements may appear incremental individually, but collectively they reinforce the view that the company is steadily advancing toward manufacturable integration rather than remaining confined to isolated technical demonstrations.

Just as importantly, management’s commentary has increasingly shifted toward integration, scalability, repeatability, yield improvement, and foundry compatibility rather than purely technical validation.

That distinction matters.

It is also worth noting that Aeluma disclosed both the Tower and Sumitomo relationships long after the underlying engagements had already begun. That reflects a notably understated and non-promotional management style. Investors expecting aggressive investor relations campaigns, flashy projections, or exaggerated commercialization timelines will likely continue to be disappointed. That has never been how this company communicates.

For this quarter, I believe investors should focus less on headline revenue and more on commentary surrounding process maturity, customer engagement, qualification progress, scaling efforts, repeatability, yield improvement, and integration into standard semiconductor manufacturing flows.

My expectation is that the quarter itself will likely appear fairly uneventful financially. That is not necessarily bearish.

Aeluma also remains my largest position, and I do not intend to trade around this quarterly report. My focus remains on whether the underlying infrastructure transition continues progressing over a multi-quarter horizon rather than reacting to short-term volatility or a single earnings release.

Over the next several quarters, the real indicators of progress will likely involve evidence of repeat customer engagement, qualification milestones, manufacturing consistency, and broader integration into commercial semiconductor workflows.

At this stage, the real signal is whether the infrastructure transition continues advancing quietly beneath the surface.

That remains the core question.

Subscribe

This publication focuses on high-signal analysis across AI infrastructure, optical networking, semiconductors, synchronization economics, and asymmetric technology transitions.

Subscribers receive:

• Deep-dive infrastructure research

• Earnings and industry analysis

• Optical networking and photonics frameworks

• Semiconductor supply-chain positioning

• Ongoing coverage of distributed AI infrastructure and synchronization economics

The goal is simple: identify where bottlenecks, scarcity, and value migration are occurring across the AI stack before those shifts become broadly understood by the market.

No noise. Just signal.

Disclaimer

This content is provided for informational and educational purposes only and should not be construed as investment advice or a recommendation to buy, sell, or hold any security.

The views expressed are solely my own and are based on publicly available information, industry research, and personal analysis. I currently hold positions in companies mentioned throughout this publication, including Aeluma (ALMU), and may buy or sell securities at any time without notice.

Investing in equities — particularly small-cap and emerging technology companies — involves substantial risk, including the potential loss of principal. Readers should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions.

No representation or warranty is made regarding the accuracy, completeness, or timeliness of the information presented. Forward-looking statements and projections are inherently uncertain and subject to change without notice.

Thank you Richard.

I think a point worth highlighting--as you have done--is that this is not a stereotypical semi small cap. Namely, instead of being out there with the front foot with press releases, developments and promises--these buys keep things close to the chest--probably too close. I think you captured that well with your words on the Tower/Sumitomo/4M award(s) release. How much more understated can you be than burying at least four (how many is awards?) in one press release?

Whether one thinks that is bad or good--it does require people to calibrate their analysis and look a bit deeper.

Great framing once again, Richard. I think we may be gearing up for a classic “sell the news” event unless there’s a major partnership announcement or meaningful progression with a Tier 1 engagement.

A lot of new eyes are on the company right now — many of which probably don’t yet understand management’s style or the timelines typically involved at this stage. As you said, the key thing right now is continued progress and validation, not suddenly posting millions in commercial revenue overnight.